|

Dipayan

Ghose never knew too much about the stock markets; that there

was money to be made in the nooks and crannies of Dalal Street.

Then the benchmark index, the 30-share Sensex, hit 8,500, and

Ghose suddenly realised that all those around him were rolling

in the moolah. Determined not to be left out, he picked up one

of those tip-sheets from his neighbourhood vendor, where he came

across this gem of advice: "If you're a newcomer to equities,

your best bet is to take the mutual fund route." That equity

mutual funds have been clocking handsome double-digit returns,

reinforced Ghose's belief that this was the most prudent way for

him to pile up a hoard. He managed to lay his hands on an application

form for a new fund offering of an equity scheme from a fund that

boasted annualised 66 per cent returns as on September 30 on its

other older stock offerings. Ghose filled up the form, opted for

the growth option (who wants dividends, he shrugged), tore out

a cheque for Rs 50,000 and put in his application at the authorised

collection centre in the first week of October. By the end of

the second week, the Sensex was in freefall, down some 500 points,

and equity schemes were in the red by 3 per cent. Ghose was worried.

Ghose (not his real name), and thousands

like him, would have had ample reason to be concerned last fortnight.

For, as the indices continued to hurtle downwards -at the time

of writing the Sensex had fallen to 8,201.73, a slump of 620.11

points from its peak-a good number of them who invested in equity

schemes would have realised that their (plummeting) stash was

locked in for three years. Only after that period could they ponder

redemption. But if Ghose and his ilk are sporting furrowed foreheads,

the Indian mutual fund industry isn't complaining at all. Reason?

Assets managed by the Indian mutual fund industry grew 30 per

cent in the first eight months of 2005, over the entire of 2004.

Even better news: Assets of equity schemes managed by mutual funds

jumped 67.5 per cent to Rs 55,743 crore in the same period. Inflows

via equity new fund offers (NFOs) in the April-September period

have already hit 16,500 crore (as against Rs 13,250 crore in the

entire 2004-05 fiscal), and to top that, there are at least 16

more nfos in the pipeline (including four new tax-saver funds).

|

|

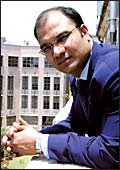

Investors are knocking

the doors of mutual funds for investing in equity markets

Pankaj Razdan

CEO, Prudential ICICI AMC |

Because of lack of

depth in the market, Sachdev is focussing only on the top

100-200 stocks

Sanjay Sachdev

MD & CEO, Principal PNB AMC |

Says Sanjay Sachdev, MD & CEO, Principal

PNB AMC: "Lower assured returns due to falling interest rates

and the lack of investing opportunities in other asset classes

have resulted in investors getting attracted towards equity-and

they are taking the mutual fund route." Adds A.K. Sridhar,

Chief Investment Officer, UTI AMC: "New investors are tapping

the equity markets through mutual funds." Sure enough, if

investors are queuing up for application forms, it's also because

they've been voyeuristically viewing the returns being dished

out by the equity fund bunch. For the first eight months of 2005,

equity schemes recorded a weighted average return of 24.4 per

cent, in the process outperforming the returns of the Sensex and

the bse-500 (which recorded an absolute return of 18 per cent

each). The increasing thrust on equity-as of December, equity

schemes accounted for 22.11 per cent of mutual fund-managed assets;

by August that figure had shot up to 28.47 per cent-has also resulted

in MFs accounting for 4 per cent of the turnover on the BSE and

the NSE, as against 2.5 per cent six months ago.

The anxiety that prevailed last fortnight,

however, revolved around whether the new flock of mf investors

had got their timing all wrong. After all, if the stock markets

slip into a deep correction, it will wash away a chunk of the

gains of the newly-launched schemes. Points out Rajiv Shastri,

CEO, Sahara Mutual Funds: "Investors who are rushing in to

capitalise on the rising market and investing big money in NFOs

(new fund offers) are carrying an immense risk in their portfolio."

That's the investor's headache. Shastri adds

that the fund manager, too, comes under a lot of pressure at such

times, and that's when "the discipline of investing in equity

markets is lost". To be sure, most funds are sitting on an

average of 10 per cent cash (see So Where Will the Cash Go?),

with some like Deutsche Alpha Equity Fund and Birla Index fund

cushioned by 46.24 per cent and 40.14 per cent, respectively.

In a correcting market scenario, fund mangers typically use up

these funds to buy stocks at lower prices, thereby lending support

to the markets.

| SCHEMES IN THE PIPELINE |

|

ABN Amro - ELSS

Benchmark Exchange-Traded Funds linked to Sectoral Indices

Chola ELSS

Deutsche Flagship Equity Fund

Deutsche Infrastructure Fund

Deutsche Stable Growth Fund

DSP ML Small & Midcap Fund

Fidelity Tax Advantage Fund

Franklin India Smaller Companies Fund

HSBC Incredible India Fund

ING Vysya Contra Fund

Kotak ELSS

Principal PNB Large Cap

Prudential ICICI Services Fund

Standard Chartered Imperial Equity Fund

Tata Contra

Source: SEBI

|

But if inflows from the foreign institutional

investor (FII) brigade dry up-in the current month till October

13, the FIIs had sold Rs 964 crore of equities on the Indian markets-can

we expect mutual funds to fill in the breach? The FII stash is

bigger, but mutual funds aren't far behind: Foreign investors

in the January-October period have poured Rs 36,500 crore on Dalal

Street. Mutual funds meantime have mobilised Rs 24,000 crore through

new equity offers in 2005, with nearly 60 per cent, or Rs 14,300

crore being fresh money (the rest can be accounted for by investors

churning their portfolios and mark-to-market gains from equity

schemes). Sahara's Shastri explains that even if 25 per cent of

those fresh inflows are retail monies, it's a significant number.

Ved Prakash Chaturvedi, Managing Director, Tata Mutual Fund, is

more sanguine. He estimates that 80-85 per cent of the increase

in mutual fund assets is courtesy of fresh flows. "Of this,

retail inflows (including high-net worth clients) account for

65-70 per cent of the inflow in equity schemes," he adds.

The interest from retail investors is clearly

visible in the increase in the number of applications for new

NFOs. For instance, in June, Principal Junior Cap Fund received

75,000 applications and mobilised around Rs 440 crore. The latest

NFO to close, SBIMF's Multicap Fund, received 3.75 lakh applications

and mobilised Rs 2,100 crore. And Tata Mutual's Chaturvedi says

he's expecting nearly 3.5 lakh applications for the Tata Contra

Fund.

|

|

The lack

of opportunities in other asset classes is prompting new investors

to tap equity markets via mutual funds

A.K. Sridhar

CIO/UTI AMC |

Fund

managers are advising investors to have a three-four year

horizon. Chaturvedi discourages investors even against one-year

investment horizon

Ved Prakash Chaturvedi

MD/Tata Mutual Fund |

That projection may just go a bit awry if

investors tighten the purse strings, sensing (yet another) bull

run going bust. The funds, for their part, might have an ideal

product for such a situation: The Systematic Investment Plan (SIP)

option, which not just reduces exposure to high-risk (by nature)

equities, it also helps the investor garner more units when the

market tanks. The sip operates like a recurring deposit of bank,

with the investor parking upwards of Rs 500 per month with the

fund, for which he gets in return his units. If he has Rs 5,000

to invest per month, he can divide that amount into five parts,

and invest at five different dates, thereby allowing him to take

advantage of market volatility.

Yet, sips on their own are inadequate protection

for fund investors, many of whom tend to join the party at the

peak of a rally. Realising the disastrous consequences these could

have on their schemes-by way of large-scale redemptions-fund managers

are advising investors to have a three-four year horizon. Says

Principal's Sachdev: "We do not want money for the short

term. Secondly with lack of depth in the market, we are focussing

only on the top 100-200 stocks. The long-term trend is intact,

but at current levels, stability in a stock is crucial and most

of the funds are not comfortable with small stock." Tata's

Chaturvedi says he's been discouraging investors with even a one-year

investment horizon during the Tata Contra Fund roadshows.

Of course, there will always be investors

looking to make quick profits, which results in them flitting

from one fund to the other, resulting in a heavy churn factor,

as high as 20-25 per cent. To deal with this, funds like SBIMF

and Kotak AMC have introduced entry as well as exit load for their

new and its existing funds. "We have introduced entry and

exit load in our schemes mainly to cap our investors and to restrict

churning," says Nitin Jain, Fund Manager at SBI AMC, who

adds that excessive churning spoils the investment pattern in

the fund. However, there are industry insiders who disapprove

of such a move that makes short-term exits costlier. One such

senior official at a state-run AMC accuses such funds of profiteering,

as they receive a 2.25 per cent load on entry and a 1 per cent

load on exit.

| DISTRIBUTORS' DAY OUT |

| Almost Rs 1,000

crore-that's how much distributors of mutual funds have raked

in by way of commissions in 2005. here's how we arrived at

the figure: So far in 2005, the top 50 distributors, on an

average, have pocketed a brokerage of 4 per cent. Mutual funds

have in this period mobilised over Rs 24,000 crore from NFOs.

Exact figure: Rs 960 crore. A senior official at a MF distribution

arm reveals that in some cases the brokerage inches up to

as high as 8 per cent. SBIMF recently garnered Rs 21,000 crore

for one of its schemes. According to industry sources, the

secret of its success: The 4.75 per cent average commission

it paid to its top 50 distributors. You have to wonder: Don't

higher distribution commissions translate into lower investor

returns? That's not the way to see it, frowns Ved Prakash

Chaturvedi, Managing Director, Tata Mutual Fund: "Compared

to insurance companies, our commissions are still low. If

we do not pay higher commission, they do not show any interest

in selling our products. Secondly, distributors are also expanding

and have been mobilising huge retail money from Tier-II cities." |

Such controversies notwithstanding, it would

appear that the Indian mutual fund industry has hit an inflexion

point-or at least the equity schemes have. As Pankaj Razdan, CEO,

Prudential ICICI AMC, explains: "This time round, for the

first time, investors are knocking the doors of the mutual fund

for investing in the equity markets. And the inflows are also

coming into existing schemes. Leaving aside the top five metros,

35 per cent incremental inflows into funds are coming from Tier-II

cities." In the US in the nineties, huge money poured into

mutual funds from us households, even as they became even bigger

net sellers of stock (from sources other than mutual funds). If

Indian mutual funds are able to ride out the current short-term

blip, and dish out handsome returns to investors over the next

2-3 years, those rewards would go a long way in introducing many

more domestic households to the mutual fund cult.

|