|

"The

industry has not been able to cost-effectively service a huge

market"

Sandeep Bakhshi

MD & CEO/ICICI Lombard |

If

Indians don't seem to care much about insuring their lives, they

care even less about their assets. Or at least that's what the

numbers reveal. Take a look: 99 per cent of the households are

uninsured, and so are 80 per cent of two-wheelers in India, and

only 2 per cent of the total health spends in the country come

via insurance. "It's more a supply side issue rather than

a demand issue. We have not been able to cost-effectively service

a huge market," says Sandeep Bakhshi, MD & CEO, ICICI

Lombard, one of the most aggressive private insurers in general

insurance.

Cost is increasingly becoming a critical

issue in general or non-life insurance. Three crucial portfolios

were de-regulated earlier this year that had a fall-out on the

overall portfolio of non-life companies. Earlier, pricing was

fixed for fire, engineering and motor insurance at levels higher

than commensurate risks. In this scenario, the insurance companies

used to cross-subsidise their loss-making portfolios with those

offering fat margins. But with tariff restrictions gone, a risk-based

pricing, de-linked from other portfolios, was expected to emerge

in the market. While that has happened in some portfolios-like

in the case of health and motor-the immediate impact was expected

to be an over-the-board drop in prices.

On that count, the consumers have not been

disappointed. Rates for fire and engineering covers have dropped

by 25 to 30 per cent. In fact, the price competition has been

so intense that IRDA has had to step in to set a floor level for

the drop in prices. "On a month-to-month basis, discounting

has doubled since February," says Kamesh Goyal, head of Bajaj

Allianz General Insurance, another aggressive insurer in the market.

Industry watchers point out that the pricing pressure is so severe

that in some cases discounts have touched 50-70 per cent as well,

although the overall scenario is still not that bad. "The

Indian market has behaved largely along expected lines and quite

well post-detariffication," says Praveen Vashishta, CEO &

MD, Howden India, an insurance broking firm.

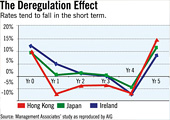

He also points out that the Indian experience

looks quite similar to those of other countries that freed up

general insurance. For example, in countries such as Hong Kong,

Japan and Ireland, the market growth suffered in the first four

years of deregulation, but that was followed by a sharp recovery

in the fifth year (See The Deregulation Effect). That means in

the short term, things will only get worse for general insurers

in the country.

Hurtful

Competition Hurtful

Competition

While customers may relish the price war

(many of the large ones are flexing muscle to get hefty discounts),

it's not in their interest in the long term-especially, if the

profitability of the insurer gets affected. If the insurer is

not healthy, then the very reason for taking an insurance cover

gets defeated, since a financially precarious insurer may be in

no position to pay claims. "The current price reductions

have no rationale as there is no perceptible drop in risk associated

with those policies," points out G.V. Rao, Chairman GVR Risk

Management Associates. Rao, a former chairman of government-owned

Oriental Insurance, believes that these cuts come from a mentality

of chasing market share at any cost. "In a bad year, with

any unforeseen catastrophe, things could become very, very ugly,"

warns Goyal of Bajaj Allianz.

Notwithstanding these concerns, Goyal expects

the pricing pressures to continue for the next couple of years.

The options are simple: chase growth or profitability. "We

have taken a decision not to focus on topline this year but to

try and defend our market share of around 7.2 per cent,"

says Goyal, adding pragmatically that in portfolios where the

loss ratios are good, the company continues to compete on price.

Otherwise it lets the business go. These pressures are evident

in the latest statistics, where the monthly growth rates of premium

for the companies have dropped to around 10 per cent as compared

to over 20 per cent earlier. This drop is despite the fact that

there has been an increase in the premium of some portfolios such

as motor vehicles.

Retail Focus

|

"What

we are selling is peace of mind and there is enough buying

power for that"

Ajit Narain

MD & CEO/IFFCO-Tokio General Insurance |

Next April, when the regulator is expected

to completely free pricing and allow changes in policy wordings,

the dynamics of the industry will change further. The prospect

of even stiffer competition has got insurers to consider growing

new lines of business. Since the squeeze on margins is particularly

severe in corporate and commercial lines of business, insurance

companies are now looking to tap retail customers to cushion against

the pricing pressures. Ajit Narain, MD and CEO of IFFCO-Tokio

General Insurance, says that nearly all companies have started

looking at retail portfolios in a big way. IFFCO-Tokio's focus

on retail business itself is such that it requires a 100 per cent

subsidiary purely for retail marketing.

Another move is towards the hinterland or

non-urban India. "Anything that is not categorised as Class

A, B or C cities is interior India for us, and that is a huge

opportunity for us (non-life companies)," says IFFCO-Tokio's

Narain. Already, the share of fire and engineering is going down

in the overall portfolio mix of insurance companies. Further widening

of the portfolio mix and, therefore, risk, makes for sound business

sense. Ultimately it will be back to the basics. Ultimately, "the

core product that insurance companies sell is risk management,"

says Rao. Adds Narain: "What we are selling is peace of mind

and there is enough buying power for that."

What will keep the general insurers going

is the fact that there's plenty of room to grow. Vashishta says

that for non-life business to contribute even 1 per cent of the

GDP, it would need to grow at 30 per cent a year for several years.

Down the road, several other changes may occur. Besides the inevitable

industry consolidation, customers-particularly companies-will

look at insurance from a risk management perspective. After all,

global warming and terrorism are changing the world in unpredictable

ways.

|