|

Last

fortnight, south african breweries (SAB) acquired Miller Brewing

from Philip Morris for $5.6 billion (Rs 27,440 crore), and in the

process became the world's second-largest beer company, after Anheuser-Busch,

the makers of Budweiser. And there could be more action on the acquisition

front from SAB: it is now reportedly eyeing another global beer

major Scottish & Newcastle (S&N), which could result in

the creation of a SAB-Miller-S&N brewing powerhouse.

The repercussions of a SAB-S&N alliance

will instantly be felt back at home. Reason? Vijay Mallya's United

Breweries (UB) has S&N as a 26 per cent partner. A global partnership

between S&N and SAB could well provide the South African brewer

with a toehold in the UB camp, which today dominates the Indian

beer market with a marketshare of just under 40 per cent.

There's scope for further consolidation too

in the 70-75 million case (a case is typically 12 bottles) Indian

beer market. Shaw Wallace, which controls 27 per cent of the beer

market, has decided to bring in a strategic ally into the brewing

business, by selling a 26 per cent holding. SAB, along with Heineken

and Carlsberg, is in the race for this holding too. Clearly, recent

activities in the Indian beer market are more than just froth.

UB, which has been on a shopping spree in recent

times could soon find itself going toe-to-toe, eyeball-to-eyeball,

mug-to-mug, with SAB. Throw in Shaw Wallace, which is in the news

for its efforts to find a strategic partner- read that as global

strategic partner-for its beer business into the script and the

result is a heady cocktail of competition and more competition.

|

| UB's

Vijay Mallya has decided it's worth sacrificing short-term

profitability on the alter of long-term competitiveness. |

Battle Of The Beer Barons

Since its entry into the Indian market 21 months

ago, SAB has been on an aggressive acquisition spree, picking up

9 million cases of capacity in regions ranging from Uttar Pradesh

to Bangalore to Rajasthan to Aurangabad. UB may still be king by

a long way, with a total capacity of 63 million cases, but the sheer

speed at which the newest entrant into the Indian beer market is

moving, coupled with the alliances taking place overseas, should

have the Indian beer baron worried.

As things stand today, the battle for the beer

bottle appears to be a two-horse race: not so much between the current

No 1 and No 2-UB and Shaw Wallace-but between the No 1 and SAB.

Industry sources don't rule out the Chhabria company eventually

exiting the beer business to focus totally on liquor.

There's Mohan Meakins with a 12 per cent share,

but it's only a matter of time before SAB, which already has 7 per

cent of the market in the bag, creeps ahead. Another MNC in the

race, Foster's India, is moving cautiously, which explains why it

has only a 2 per cent share. However, the company's recent aggressiveness

in Delhi-the market, quite literally, is flooded with the Australian

beer-puts a whole new slant on its articulated strategy of seeking

opportunities.

The regional players control a vital 13 per

cent, and indeed could be ideal takeover candidates for both SAB

and UB. SAB for its part is convinced that the acquisition route

is the quickest way to race ahead of the pack. As Richard Rushton,

Managing Director, SAB India, puts it: "Consolidation through

acquisitions is important in India because setting up a greenfield

brewery, despite the advantage of brewing the beer you know, proves

uneconomical in the long term."

So is UB worried? Well, yes and no. Ravi Nedungadi,

President & CFO, UB Group, is aware of SAB's reputation of injecting

economies of scale into the brewery business. But he feels the Indian

market is a different mug of beer. "To squeeze out efficiencies

from the far-flung breweries of India is not possible... (what's

more) they do not have a class brand... so we are confident of taking

them on and winning," adds Nedungadi.

|

| SAB's

Richard Rushton is convinced that the acquisitions route

is the quickest way to race ahead of the pack. |

The unique nature of the Indian markets is not

lost on Rushton. He concedes that making small breweries won't be

easy. That's why he's talking about "critical mass, so that

costs can be brought down and the brand developed at the front end."

The battle may be one of just words as of now,

but it will soon wean its way into the beer drinking markets of

the country-which can only expand.

For, the scope for increasing consumption of

beer in India is enormous. In the US and China, for instance, consumption

of beer stands at 220 and 215 million hectolitres, respectively.

In India, it's still just 5.5 million. The

good news, though, is that the domestic market is growing at 10-12

per cent per annum, even as most developed countries have reached

stagnation levels.

So although UB may be head and shoulders above

the rest, the potential for growth that exists in the domestic market

can easily tilt the scales in favour of a new brewer in town.

Of course, increasing beer consumption won't

prove the easiest of tasks, thanks to high prices, distribution

hurdles, and consumer perception. As Deepak Chaudhuri, Director,

Shaw Wallace Breweries, observes: "In view of the high unit

price of beer, a large chunk of beer consumers have turned to hard

liquor leading to stagnation in the industry."

In India, then, beer competes with hard liquor,

which isn't quite the case in developed markets, or developing markets

like China, where it is largely up against soft beverages for share-of-sip.

Also, beer is not too economical to transport,

which explains why manufacturers prefer to have a brewery close

to market. Explains Pradeep Gidwani, Managing Director, Foster's

India: "Every state in India levies different taxes, resulting

in small, inefficient breweries across key markets, and since moving

inter-state is not possible, it is not profitable to bank merely

on a handful of units." For example, a 650 ml of Foster's in

a Maharashtra vend costs Rs 50 and the same retails in Delhi for

Rs 35.

|

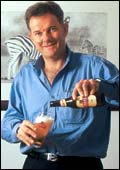

| Foster's

Pradeep Gidwani is looking for strategic and focussed

growth opportunities across the sub-continent. |

On An Acquisition Spree

All these bottlenecks haven't deterred UB from

hitting an acquisition trail of its own. It has little choice, for

it has to pre-empt SAB. Mallya too, like Rushton, isn't keen on

greenfield projects because of the longer gestation period involved,

which could go up to two years-which is a long time in the beer

business.

UB hasn't been afraid to put its money where

its mouth is, by pumping all of Rs 100 crore into acquiring the

Chennai-based Empee Breweries.

Clearly, Mallya has decided it's worth sacrificing

short-term profitability on the altar of long-term competitiveness.

His beer company made a Rs 56-crore loss last year, which the CFO

attributes largely to the acquisitions. "In the past two years

we have made investments of nearly Rs 350 crore in acquiring additional

capacity," explains Nedungadi.

Mallya needs to mop up as much capacity as

he can. For, if No 2 Shaw Wallace falls in the hands of a global

major, UB's numero uno position would, at a stroke, come under threat.

Shaw Wallace, meanwhile, is on its own expansion spree, going after

only capacities, not brands. Over the recent past, the Chhabria

company has amassed seven wholly-owned breweries and 14 contract

manufacturing units.

Says Chaudhuri: "We have entered into

contract arrangements with a number of brewers nationally to roll

out our brands." The thinking at Shaw Wallace is that, in view

of the ban on liquor advertising, it makes more sense to increase

the volumes of existing bestsellers and thus capture a larger chunk

of the market. That explains why Haywards 5000 has been able to

grow by 35 per cent last year.

The Importance Of Alliances

Shaw Wallace, though, has realised that tying

up with a global beer major makes more strategic sense than slugging

it out against the MNCs without a partner. And it's not alone in

sUBscribing to that train of thought.

There's Mount Shivalik Industries too that has

taken a similar tack by opting for a strategic tie-up with Stroh's

International. Reaffirms Monish Bali, Director (Marketing), Mount

Shivalik, which makes Thunderbolt, a popular strong beer brand in

North India. "It is impossible to fight foreign players unless

you have deep pockets and so we've tied up with Stroh's." He

doesn't fail to add: "From all accounts, it seems UB is the

only local brewer who has what it takes to pose a formidable challenge

to the MNC brigade." With some assistance from a MNC, Scottish

& Newcastle.

Internationally, beer is a highly evolved business

and therefore, demand-led. Brands flank across borders and people

know the beer they're drinking. In India, where the market is still

at a nascent stage and highly fragmented, demand orientation seems

a long haul. For the moment, capacity is the name of the game. And

SAB and UB are worthy contenders for the biggest draught of Indian

beer.

-with additional inputs from

Venkatesha Babu

|