|

|

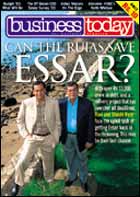

| Not out of the woods yet: (Clockwise

from bottom right) Essar Group's Ravi Ruia, Shashi Ruia, Anshuman

Ruia & Prashant Ruia |

It's

a new day at the mouth of the Tapi river, roughly 25 km off Surat,

towards the tip of Hazira's bustling industrial belt. The tide has

ebbed, and a wintry but gentle breeze drifts across the jetty built

by the Ruias of the Rs 5,700-crore Essar Group as a part of its

2.2 million tonne steel plant. On the wharf, gazing into the distance,

is Captain S. Das, Vice President (Operations), Essar Shipping,

who's running a film of the day's export shipments in his mind.

In a yard adjacent to the port, hundreds of hot rolled coils of

varying sizes (ranging from 10-25 tonnes) sit neatly side by side

in zones earmarked by destination. One placard dug into the ground

says Jakarta, another China, and yet another Dammam (in the Middle

East). Giant cranes are loading the coils onto mini-bulk tugs that

are docked at the jetty. By afternoon the tide will come in, and

these small ships will steam across to the high seas, where two

giant floating cranes will load roughly 3,000 tonnes of steel onto

a bulk carrier of 110,000 tonnes. By March 31, 2003, roughly 40

per cent of 1.8 million tonnes of steel produced by Essar in the

current year would have moved into overseas markets via this route,

making it the largest Indian exporter of flat steel. Also, 1.8 million

tonnes will be the highest Essar's steel plant has ever been ramped

up to.

Since the plant came on stream in 1996, the

Ruias haven't had too many opportunities to indulge in such production

and export step-ups. Only a year after production started, steel

prices slipped into an unforeseen free-fall, eventually hitting

a 40-year-low of $160 per tonne. For the highly-leveraged Essar

Steel-its total debt stands at Rs 5,400 crore-this spelt disaster,

as interest costs as high as Rs 650 crore a year ate into whatever

meagre profits it could show at the operating level. Factor in the

meaty depreciation charges and it is easy to see why the accumulated

red on the books stands at a little over Rs 1,700 crore. Defaults

on interest payments didn't invoke any sympathy, either.

If the steel history sounds hopeless, the four-year

delay in the Ruias' ambition of putting up a 12 million tonne refinery

off the Vadinar coast in Jamnagar, Gujarat, completes a truly despairing

picture. As of date, at least 36 per cent of the engineering, procurement

and construction is yet to be completed since work on the project

stopped in 1999. Result: A cost overrun of at least Rs 2,000 crore,

and a debt exposure of close to Rs 5,000 crore, even as neighbour

in Jamnagar, one Reliance Petroleum, contemplates an expansion from

27 to 40 million tonnes.

Here's some perspective into the group's plight:

Most of its Rs 7,625-crore earnings before interest between April

1996 and March 2002 have been virtually wiped out by interest and

principal payments of Rs 4,500 crore and Rs 3,200 crore, respectively.

Let's put it this way: If even one of these two mega-projects (steel

and refining) doesn't pan out, that failure will be enough to sound

the death-knell of the Essar Group, whose total debt exposure stands

at a staggering 13,800 crore. To be sure, the Ruias have already

been written off by the stockmarkets, and by most of its 13 lakh

shareholders, from whom the Ruias have cumulatively raised close

to Rs 3,000 crore.

| Not everybody believes that falling commodity

prices and burgeoning costs did them in. Charges of siphoning

off publicly-raised funds have persisted over the years. |

Not everybody believes that just falling commodity

prices and burgeoning finance costs did the group in. Charges of

siphoning off publicly-raised funds and manipulation of the institutions

have persisted over the years. As a result, the perception has gained

ground that the Ruias are nothing more than thieves in pinstripes.

The swank 21-storey blue-glass Essar House-in which the brothers

Ruia sit at two ends of an office on the 20th floor that's as big

as a tennis court-and an office-cum-residence on the outskirts of

New York juxtaposed against dismal results and unrewarded shareholders

only perpetuate that perception. As do the fast cars-Shashi and

Ravi drive Jaguars and Shashi's youngest son Anshuman a bmw. And

a two-storey bungalow overlooking the sea in Mumbai's upscale Walkeswar

(the Ruias stay in four individual apartments in that bungalow,

which has one common kitchen). Or Ravi and Prashant's nri status

and a farmhouse in the hills of Lonavala. And a plush Delhi office-cum-residence

in Jorbagh...

"The feeling is that although shareholders

have been hit badly, the lifestyle of the Ruias hasn't in the least,"

points out a fund manager. "It's time for the government to

change the management. The truth is, they are known defaulters.

Whether they are willful defaulters or useless entrepreneurs I cannot

say, but they could well be both," adds Amar Singh, General

Secretary, Samajwadi Party.

The Ruias for their part have left no stone

unturned to absolve themselves of the numerous charges hurled at

them, many of them by Amar Singh. And those clean chits have been

pouring in, right from the Central Vigilance Commission to the fm

to the Law Minister. But the best way for the Ruias to counter those

charges is by performing. What could help them do just that is the

few silver linings that have appeared on the huge dark cloud threatening

for some time now to burst over Essar House.

| A matter of emphasis for the Ruias is that

their other businesses--construction, power, telecom, and shipping--are

all in clover |

For starters, the Ruias got a major shot in

the arm when the institutions' corporate debt restructuring committee

(CDR) agreed to rejig the Rs 15,000-odd crore debt of the steel

industry. Essar Steel, which has a Rs 3,200-crore exposure to the

Indian FIs, can now convert 40 per cent of that amount into lower-cost

foreign debt. Not just that, the average interest rate on their

total exposure has been dragged down into the 11-12 per cent range,

as against 16-19 per cent earlier, and the tenure of the loan has

been extended to 13-15 years. Coupled with rising steel prices and

a proposed buyback of the existing foreign debt at a 70-75 per cent

discount, the Ruias expect this restructuring to help them not just

make profits in 2003-04 but also wipe out most of their accumulated

losses.

Points out B.P. Singh, Chief General Manager,

IDBI: "Steel prices are moving up, and the projects look viable.

If they weren't, we wouldn't be restructuring the loans.''

"We're there in steel," beams Shashi

Ruia, the 58-year-old Chairman and architect of the group's core

sector blueprint. With prices expected to hold at the $340-350 a

tonne-levels the Ruias are projecting a gross profit of Rs 700-800

crore in 2003-04, and the CDR recommendations coupled with the debt

buyback proposal, will bring down the interest burden from Rs 650

crore to Rs 350 crore. What's more, if the Ruias do succeed in buying

back most of their Rs 2,200-crore foreign debt at a 75 per cent

discount, they would have knocked off Rs 1,400-1,500 crore off their

books, which can be set off against the accumulated losses on the

balance sheet straightaway. Result: A clean slate.

|

|

| FINANCE MINISTER JASWANT SINGH

AND FORMER FM MANMOHAN SINGH (L TO R) |

| Clean chits have been pouring in

from all quarters---from the CVC to the present and former FMs

to the law minister |

Sleepless In Jamnagar

If the steel project is finally looking viable,

the 12 million tonne refinery is at last beginning to look a reality.

For four years now, the only action at the site of the Ruias' proposed

12 million tonne refinery has been the maintenance and monitoring

of the equipment procured. That delay has been thanks largely to

an equity gap of Rs 582 crore and the FIs' subsequent decision to

clamp down on disbursements. In the lavish 21st floor dining room,

over a spartan salad lunch-Shashi's sons, Prashant and Anshuman,

nibble on an equally austere vegetarian thali as they listen on-Vice

Chairman, Ravi Ruia (54), spells out the reasons for the hope brewing

on the Vadinar horizon.

The first of those can be summed up in two

words: 9 per cent. That's the rate at which the institutions might

just about be willing to recommence disbursements-Rs 1,000 crore

has yet to be disbursed-to the Ruias. If ICICI Bank (the lead institution,

whose officials refused to comment on the issue) does agree to that

rate, it will be a huge triumph for Essar Oil, which has been accustomed

to borrowing at 20-21 per cent in the late nineties. Then, ABB,

the EPC contractor for the refinery, has agreed to temporarily bridge

the equity gap of Rs 582 crore (which it will be free to sell later

on to a strategic partner) in the project. ''Our equity is tied

up, loans are in place. Take into account a sales tax deferral,

and we're back,'' says Ravi Ruia, who expects to commission the

refinery 24 months from the day work starts, which could be anytime

now. The Ruias also stress that at the proposed interest rate, the

project looks immensely viable: Cash break-even according to projections

should happen at 35 per cent utilisation, and break-even after interest

and depreciation at 65 per cent.

Another matter of emphasis for the Ruias is

that their other businesses-construction, power, telecom, and shipping-are

all in clover. For shipping, in which the Ruias own 33 ships (including

six of the world's 80 double-hulled, double-bottomed Suezmax tankers),

freight rates are on the up. Power is an assured business thanks

to a 20-year purchase agreement with the Gujarat government. A 36-37

per cent partner in the consolidated cellular telecom operations

of Hutch (which will hold 49 per cent) will assure the Ruias decent

returns on their Rs 500-crore investments. In construction, Essar

has Rs 1,000 crore of orders in hand, the major one being a section

of the National Highway in the South. And in oil, Essar hopes to

put up 1,700 retail outless via the franchise network, and upstream

the group is exploring 14,000 sq km for oil and gas and coal-bed

methane. The Ruias feel that because of their huge exposure to institutions,

the fact that they've created world-class assets worth over Rs 17,000

crore gets overshadowed.

It's still too early to begin writing tales

of a turnaround at the Essar Group. The 'ifs' are many, one of the

biggest being the foreign lenders' willingness to allow the Ruias

to buy back debt at a huge discount. Clearly, it will be many more

years before the Ruias are able to steady the ship and even many

more before they can reward shareholders. But then there's no other

way out: Much of the group's equity is lying pledged with the FIs,

which might just be willing to consider Amar Singh's painful recommendation

if the non-performance persists. The good news for the Ruias, though,

is that the tide is turning. Their time starts now.

1

2

|