|

I'd

like it to be a complete surprise. On the day I turn 40, I'll go

into work early, send a bulk mail with something as cool as Chatwin's,

"Off to Patagonia", maybe something nastier made-to-order

for the boss who steals all my ideas and hogs all the credit, stop

at the city's only excuse for a park, take off my shoes and let

the grass tickle the soles of my feet, and return home and wait

for the significant other. I will do nothing with my time other

than read, write (if it isn't too much work), drink in moderation,

exercise, again in moderation, and practice vegetating. You see,

I plan to retire at 40.

I can do it; time is on my side-I am just 31

now, don't have any debts against my name or any outstanding credit

card bills, or parents who need to be supported. I have it all worked

out in my head: the amount I'll need to maintain my altered lifestyle.

If I am not going to hold down a job, I certainly won't have to

spend a few lakhs of rupees every year on being well-clad and well-shod.

A few 501s will do. As will some regulation sneakers. And I am told

both can be acquired at sales.

I won't need a driver. If I am going to be

at home, I might as well drop the kids at school, pick them up,

drop them at the tennis club, pick them up, drive them to their

music lesson.... The cook can go too. I have always liked to cook

and I am willing to bet my last salary cheque that this will bring

down the grocery and vegetable bill.

There's still the kids' education, medical

expenses, planned and unplanned, vacations, clothes and toys for

the kids, loose change (if you could call it that) for books and

music-I don't know if I can keep that Amazon.com habit going after

40-and utility bills, but if I invest wisely, and I plan to, these

should be a breeze. Patagonia, here I come.

THE FAMILY MAN

Exxon Mobil Exec, Vineet

Thacker dreams of an idyllic (early) retirement.

AGE: 31

INCOME: Rs 800,000 p.a.

EXPERIENCE: 9 years |

| Thacker is as

organisation man as they come. He insists that we run a caveat

that his views on early retirement and how he plans to achieve

it are his own and not Exxon Mobil's. Done. Thacker will probably

continue working after 40, despite the fact that he ends up

working most Sundays, and doesn't have time to read and meet

up with friends. But the man admits that over the "next

10-to-12 years," he will "invest money in such a way

as to achieve my goal of an early retirement". That'll

mean a change in his essentially debt-oriented portfolio. Part

of Thacker's investment will go into a small house ("with

a nice garden") in a beach-resort on the limits of Mumbai,

Alibaug. Part of the house will be rented out to weekend vacationers

and serve as "an alternate source of income". That's

smart. |

THE ACTIVE RETIREE

It is still in the future, but insurance

exec Suresh Subramanium has entrepreneurial

visions post retirement.

AGE: 33

INCOME: Rs 10,00,000+ p.a.

EXPERIENCE: 13 years |

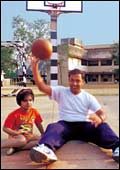

|

| The overseas model: Zalkikar's

approach is not for everybody |

Subramanium's is the ideal retire-early

portfolio. They have always had a 60 per cent slant towards

equity and he plans to keep that ratio intact for the next 10

years. Not for Subramanium the safe mutual fund route-he invests

directly in equities, a fallout of his interest in equity research

and the stockmarket. While he is clear that he will retire early,

Subramanium is still unsure of what he will do: he could consult

for a business process outsourcing firm, extend his interest

in dramatics into a career in event management, or leverage

his interest in training optimally. One thing is certain: this

man won't vegetate. |

PART-TIME PLANNER

Software pro Makrand

Zalkikar hopes to do his own thing-six months of the

year-after retiring at 40.

AGE: 32

INCOME: Rs 750,000 p.a.

EXPERIENCE: 9 years |

|

| The equity route: Subramanium is

putting his knowledge of equities to good use |

It wouldn't do to emulate zalkikar.

his portfolio is skewed towards debt and insurance, and although

he plans to invest in some real estate, none of these can really

provide him the kind of nest egg he wants. What will, is the

fact that the man will almost certainly spend between two and

three years overseas. Zalkikar plans to put aside whatever he

saves (in dollars) and use the money to start a "small

travel business" when he turns 40. The avid para-glider

and bungee jumper wants to get into the adventure tours business.

"Ideally, this should be season and run for just six months

of the year," he says. Like we said, it wouldn't do to

emulate him. |

Let Me Tell You How

First off, get your time horizon right. According

to the Indian Government's Old Age Social & Income Security

(Oasis, I'm told is how the babus refer to this) report, a person

who is 40 can hope to live another 37 years. The report further

suggests that by 2010, this figure will be 45 years.

Me, I think I am healthy enough to see 90.

I don't smoke, apart from the occasional cigar, and that is an indulgence

I hope to retain. Liquor is restricted to the occasional glass of

single malt or wine. And I exercise regularly. That means I can

look forward to a long and indolent retirement. It also means I

can't expect my provident fund to last very long.

Fortunately, a few years after I started work-those

were the days of my dissolute youth-I read a magazine article (not

half as well-written or knowledgeable as the one you are reading)

that quoted a man called Rajiv Bajaj who headed a company called

Bajaj Capital (I am told he still does). The only Bajajs I knew

of were in the motor trade, but this man obviously knew his investments.

''A person who aspires to retire early should start saving the day

he gets his first salary,'' he was quoted as saying. I hadn't done

that, but started soon after reading the article. Six years on,

I am better off for that: money, in case you didn't know, begets

money. There were (and are) enough schemes on offer: recurring deposits,

systemic investment plans, and special insurance schemes targeting

early retirees where one pays a high premium while working and no

premium (or a very small one) post retirement.

I am not what you could call a disciplined

or organised person, but I forced myself to invest regularly. It

was painful at times-I went four years without replacing my television,

for instance, World Cup to World Cup-but I prevailed. I told myself

that a person who saves regularly would, in the long term, save

more than someone who opted for the big bang saving. I also told

myself that I was delaying my gratification. When I was 41 and watching

Harry Potter and the Order of the Phoenix on DVD, my erstwhile colleagues

would be rushing to get into work.

Temptation was never far off. Every time an

investment matured there he was, Old Nick in the flesh, standing

behind my shoulder and whispering sweet somethings into my ear:

Bose Lifestyle, Philips Plasma, or Royal Carribean Cruise. Again,

I prevailed. I stayed invested in schemes that offered recurring

benefits; mutual funds, for instance do. And I took the money out

of those that didn't and reinvested it. I am sure I will be tempted

again, and I am equally sure I will resist. As we of the Cosa Nostra

tell ourselves, Bambino, gratification is a dish best eaten cold.

...And Let Me Tell You What

I won't take too much of your time now-I have

to get back to work. There's one more piece of wisdom I'd like to

share from that article I read long ago. This one too comes courtesy

Bajaj. ''If you want to retire at 40,'' I remember him as having

said, ''your investing strategy should be built around capital growth.''

Mine is. Almost half my portfolio is in equity, some direct, and

the rest (actually, most of it) through mutual funds. After 40,

I will have the time to study and pick stocks myself. Equity may

hold some risks, but it is the one sure way to meet growing expenses,

and beat inflation. Interested?

|