|

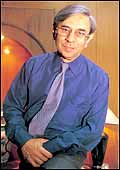

| Homi Khusrokhan, MD, Tata Tea: Growth

is where Tetley is |

Bishop

Lefroy road in Kolkata is best known for being home to Satyajit

Ray. Not surprising, then, that the ochre-yellow, two-storey building

bang opposite the late filmmaker's mansion, rarely catches a passing

eyeball. If there's anybody distressed at the slight, it's not Homi

Khusrokhan. The Managing Director of Tata Tea is getting plenty

of spotlight, thank you. Reason: His company's three-year-old, $400-million

acquisition of British premium tea brand, Tetley-a deal that was

dubbed a costly disaster soon after it was announced-is proving

to be its smartest move yet. ''I guess I could say 'We always told

you so','' chuckles the 59-year-old Khusrokhan, who previously headed

Glaxo India, before joining Tata Tea in February of 2001.

That's not an empty boast. Dalal Street, which

punished the stock pushing it off its peak of Rs 632 in January

2000 just months before the deal in March 2000 to a low of Rs 116

in September 2001, is beginning to acknowledge the value of the

deal. Since the beginning of this calendar, the stock has risen

some 70 per cent to Rs 300-the highest in 30 months. (Just for the

record, Tetley was acquired via a special purpose vehicle, Tata

Tea GB, which continues to be separate from Tata Tea.) So what's

new about the story that has D-Street all ears?

A Heady Brew

Actually nothing. It's still the story of how

a struggling tea plantation company became, in one deft move, one

of the world's biggest branded tea players. Only that now the deal

looks much more convincing. The more immediate provocation, from

the earnings-hungry investor's point of view, is the debt restructuring

that took place last day of February this year. Under the new deal,

the £171 million (Rs 1,316.7 crore) of outstanding debt, which

carried an average cost of 10.22 per cent per annum, has been swapped

with £174 million (Rs 1,339.8 crore) of fresh loans (£3

million, or Rs 23.1 crore, covers the transaction costs), borrowed

at an average cost of 6.7 per cent a year. That translates into

£6 million (Rs 46.2 crore) of savings annually-not exactly

chump change.

Crush and Curl

Since 2000, the Tatas have put Tetley

through some major restructuring. |

»

Shut down the Australian plant and shifted

production to Cochin this year

»

Sold Tetley's private label business in the US last year

»

Closed three plants in the UK and US, retaining one in the former

»

Pruned workforce from 1,500 to about 1,100 currently

»

Swapped high cost debt for low cost debt at 6.7 per cent per

annum, early this year |

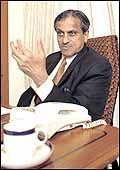

But that's only a small part of the story that

Khusrokhan and Vice Chairman R. Krishna Kumar, who put his reputation

at stake by championing what even today is corporate India's biggest

deal, are selling to their investors. The big story goes something

like this: Tea prices in India are falling (from Rs 76 to Rs 54

per kg over the past five years), loose, or unbranded, tea is muscling

out the branded players, whose marketshare has only of late inched

back to 37 per cent after dropping to 32 per cent in 1999, and per

capita tea consumption is stagnating at 650 gms. The only option

for a company like Tata Tea, which has seen its revenues and profits

shrivel (See The Big Squeeze) over the last four years, is to move

into markets and segments that are growing. Says Krishna Kumar:

''It was evident that Tata Tea had to move on and be a global player

if it was to continue on its growth path.''

As the world's biggest black tea bag brand,

Tetley-which the Tatas tried to acquire once before in 1995-brings

Tata Tea both volumes in the short term and greater opportunities

in the long term. In the UK and Canada, Tetley already leads the

market with 29.4 per cent and 43.4 per cent shares, respectively.

In Australia, it is the fastest-growing tea brand, and in the US

it has 11.5 per cent of the black tea bag market. And after moving

into Pakistan and Bangladesh, both big tea-consuming markets, Tetley

is getting its act together in the Middle East, Africa, and Russia,

where it is giving the final touches to a new distribution network.

The £6 million that it has freed up in annual cash flow will

no doubt help beef up Tetley's operations in the new and existing

key markets.

But it's unlikely that one common strategy

will work across these markets, even if they were on the same continent.

Take Europe, for example. In the UK, tea is a beverage of every

day consumption. But in France, tea is not only more expensive than

coffee but is also treated as a drink for special occasions. Thus,

while consumers in Britain may be more price sensitive, those in

France may want more exclusive products and may be prepared to pay

a premium for them.

The difference in consumption habits is no

doubt one big reason why Tetley wants to grow its non-black tea

bag business. Currently, its flavoured tea bags, fruit teas and

herbal teas fetch only 5-6 per cent (a market estimate that Tata

Tea would neither confirm nor deny) of its revenues. But Tetley's

Managing Director K. Pringle sees a huge market potential. In an

analyst conference call earlier this year, he cited the $5-billion

(Rs 22,500 crore) tea market in the US, where $3 billion (Rs 13,500

crore) of the market is for ready to drink tea, $1 billion (Rs 4,500

crore) for fruit and herbal, and only the remaining $1 billion,

for black tea. And Tetley currently only sells black tea in the

US. Therefore, to grow Tetley only has to do a good job of launching

new drinks.

|

"Tata Tea had to

move on and be a global player if it was to continue on its

growth path"

R. Krishna Kumar/Vice Chairman/Tata Tea |

Payback Time

If things are looking a lot better at Tetley

today, it's because of some major decisive moves that the new management

lost little time in making. First off, Tata Tea decided to shutter

two of its manufacturing facilities in the UK, retaining just one.

In the US, where capacity was freed up after it exited the private

label business, it turned its facility in Marietta, Atlanta, into

a joint venture with Harris Tea. In Australia, it relocated the

Melbourne-based unit to Cochin. According to Tata Tea's Director

Finance Anil Goel, the move was prompted by not so much the fact

that Cochin was cheaper as the fact that the Melbourne facility

was constrained for capacity, and instead of investing in a bigger

plant in Australia, it made sense to relocate the unit to Cochin.

Many critics expected the acquisition to falter

because of the stark cultural differences. Tata Tea was more of

a sleepy plantation-dependent company, whereas Tetley did not own

a single plantation and sourced all its leaves. Then, there were

issues relating to compensation structures and overlap in functions,

among others, that could have proved a stumbling block. But surprisingly

enough, merging the two entities operationally (legally they are

still separate) did not throw up any major glitches. Says P.T. 'Percy'

Siganporia, Deputy Managing Director, Tata Tea: ''We had been working

actively with Tetley even before the merger, so I guess the culture

issues that generally plague mergers of this scale were non-existent."

Today, the Tetley and Tata Tea teams work closely.

There are management committees that Khusrokhan and Pringle head

jointly. Task forces have also been created in areas such as marketing,

supply chain, and procurement. (Boston Consulting Group continues

to help with the integration). Tata Tea has even transferred specific

skills, such as tea buying, sourcing, and blending from Tetley.

For example, it has moved from a ''heritage system''-an old-world,

touchy-feely system-to Tetley's uniform computerised rating system,

Broadbrush. Says Siganporia: ''With Broadbrush, you don't have to

be at the buying place physically, besides it is easier to assemble

recipes. Both yield a huge jump in productivity.''

But for Khusrokhan, there's plenty of work

to be done at home. Although his company straddles the entire market

spectrum from economy to premium, HLL is still the leader with a

33 per cent share (org data for April 2002-March 2003). Then there

are regional brands and a clutch of small, nimble unbranded players

who are undercutting their bigger rivals through aggressive pricing.

Having Tetley in the fold, then, enables Tata

Tea to ride out the market troughs much more evenly. But what Krishna

Kumar and Khusrokhan want of their ''big hairy audacious growth'',

as it is referred to internally in the company, is something as

simple as the cuppa their stuff makes: To make Tata Tea the world's

largest branded tea company. And as of now, things seem right on

track.

additional reporting by Shailesh

Dobhal

|