|

THE TOP 10 BANKS

|

|

1

|

HDFC Bank |

|

2

|

Citibank |

|

3

|

ABN AMRO Bank |

|

4

|

State Bank of Patiala |

|

5

|

Oriental Bank of

Commerce |

|

6

|

Corporation Bank

|

|

7

|

Hongkong & Shanghai

Banking Corp. |

|

8

|

Kotak Mahindra

Bank |

|

9

|

Standard Chartered

Bank |

|

10

|

Jammu & Kashmir

Bank |

Early

this December, when ICICI bank's K.V. Kamath told reporters at the

sidelines of the World Economic Forum's annual India jamboree that

bank stocks were undervalued, he wasn't being wishful. After all,

last year was a good time to be a banker. Falling interest rates,

a pick up in demand for loans, especially from the retail sector,

and fat (and effort-free) profits from treasury operations meant

that the good banks got better and those positioned precariously

got an opportunity to write off their bad loans and provide for

those they hadn't. Besides, with asset securitisation making progress,

albeit haltingly, (there are three asset reconstruction companies

in India now with acquired assets of Rs 9,631 crore), there's a

new spring in the step of your friendly banker.

Take a look at what's happened at some of the

top banks. HDFC Bank, which tops the list once again this year,

has reduced its non-performing assets (NPAs) as a percentage of

total advances from 0.4 per cent to 0.16 per cent; State Bank of

Patiala, which retains its #4 slot, has wiped out the 1.5 per cent

NPAs that were there on its books last year. Oriental Bank of Commerce

has not just moved up from #8 to #5, but also got rid of the 1.4

per cent NPAs. That even as these banks grew their business between

24 per cent and 41 per cent last year.

That things are increasingly looking up for

the sector wasn't lost on Dalal Street, where bank stocks were red

hot. In the 12 months to March this year, the BSE Bankex Index rose

from 1,393 points to 2,993 points-a 115 per cent jump, compared

to bse Sensex's 82 per cent gain in that time. While it took a huge

dive in May (because of expectations of rising interest rates, policy

uncertainty and earnings risk in terms of higher agri-lending directed

by the new government, besides lower treasury profits), it has now

touched a new high of 3,495. With consolidation in the air, the

bigger banks getting ambitious still, and interest rates going up,

things can only improve. Says Punit Srivastava, Analyst, Enam Securities:

"At current valuations, near term interest rate uncertainties

are being masked by strong credit growth and stable margins."

Not surprisingly then, the 11th BT-KPMG annual

list of India's Best Banks captures this trend. Of the 59 banks

ranked this year (another 27 banks with five branches or fewer have

been ranked separately under the small bank category), five of the

top 10 have made it to the honours roll for the last three years

in a row. The four large foreign banks-Citibank, ABN Amro, HSBC

and Standard Chartered-continue to remain in the top 10 as they

capitalise, launch new products and expand their distribution reach,

and gear up to partner with an India Inc. that is going global.

(An interesting bit: A new private bank, Kotak Mahindra Bank, debuts

on the list and straightaway at the eighth position.)

|

THE TOP 10 SMALL BANKS

|

|

1

|

Deutsche Bank |

|

2

|

Bank of Tokyo-Mitsubishi |

|

3

|

JP Morgan Chase

Bank |

|

4

|

UFJ Bank |

|

5

|

Antwerp Diamond

Bank |

|

6

|

Barclays Bank |

|

7

|

Bank of America |

|

8

|

Chohung Bank |

|

9

|

Mizuho Corporate

Bank* |

|

10

|

Arab Bangladesh

Bank |

| *(Formerly The Fuji Bank) |

But are the stronger banks getting stronger

and the weaker banks falling by the wayside? On the face of it,

yes. HDFC Bank, for example, has held on to its top perch. Citibank,

which had slipped to #7 last year from being #4 the year before,

has clawed back up to the #2 position. In contrast, there's no significant

improvement in the bottom end of the list. Its denizens like Punjab

& Sind Bank, Dhanalakshmi Bank and Centurion Bank haven't managed

to deal with their NPA problems to the same extent as the other

banks. Punjab & Sind Bank's NPAs as a percentage of net advances

was a high 10.9 per cent last year, and this year it has come down

to 9.6 per cent. Dhanalakshmi's down from 9.7 per cent to 7 per

cent, but as is obvious, the figures are still too high.

Interestingly, though, some of the banks from

the middle order-especially Vijaya Bank, UTI Bank and IndusInd Bank-have

managed to catapult themselves into the top 20 this year. Consider

IndusInd. Last year, it stood at #35. This year it has soared to

the 19th position. What's happened in the meantime? Its deposits

have jumped from Rs 8,598 crore to Rs 11,200 crore, net profits

are up from Rs 90 crore to a whopping Rs 262 crore, and loan loss

cover, which is provisions for bad loans as a percentages of overall

bad loans, has improved from 14.6 per cent to 18.1 per cent. Yet,

the bank has some way to go. Its NPAs still stand at 2.7 per cent

of net advances and are growing at a rate of 9.7 per cent. Bhaskar

Ghose, the bank's Managing Director, says that things are improving.

"Focussed attention on operations and customer service, and

concentration on a select mix of businesses, efficient treasury

management and aggressive NPA management will improve things further."

Just the same, what's driving the performance

of banks like HDFC, Citibank and Corporation Bank? A mix of factors.

On the one hand, banks like these are aggressively chasing the retail

consumer and wooing her with new products and services. On the corporate

front, they are bundling services and offerings to lower transaction

costs for their clients. Plus, they are pushing third-party products

for fee-based income, since it allows them to sweat their fixed

costs. But since competition is fierce in the business, especially

in retail banking, these banks keep a sharp eye on their cost of

funds. Says Sanjay Nayar, Country Head, Citibank: "We have

been consistent in our strategy with four clear paradigms-increase

distribution and reach, sell multiple products and consolidate the

client wallet, have a keen eye on risk management, and invest keenly

in brick-and-mortar, as well as people."

The Biggest Bank

SBI beats the others hands down. |

|

"We have

good size and excellent geography in India, and we would

be interested in exploring acquisitions overseas"

A. K. Purwar

Chairman and Managing Director, SBI |

With Rs 3,18,619 crore in deposits

and average working funds of Rs 3,75,804 crore, the State Bank

of India (SBI) stands tall in the industry. The closest competitors

aren't a third as big as SBI. Punjab National Bank ranks #2

in deposits, but has deposits of just Rs 87,816 crore. ICICI

Bank is the second biggest as far as average working funds are

concerned, but that stacks up to just Rs 1,06,593 crore. SBI,

which accounts for 18 per cent of all deposits with commercial

banks in India, is able to mop up such large amounts in low-cost

deposits because of its sheer reach: it has 13,635 branches

spread all over the country. Can SBI hold on to its top slot?

For the next few years, easily. There are other bigger banks-ICICI

Bank, for one-that are growing aggressively. Last year, while

SBI's deposits grew 7 per cent, those of new private banks swelled

at 29.6 per cent. Add to it the coming mergers and acquisitions

(M&As), and SBI's position will come under threat. Says

A. K. Purwar, Chairman and Managing Director, SBI: "We

have good size and excellent geography in India, and we would

be interested in exploring acquisitions overseas." To keep

its lead, the banking elephant will have to learn to dance. |

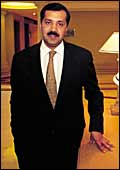

The Most Productive Bank

Not surprisingly, it's the hard-charging

Citibank. |

|

"We have four clear paradigms:

increase distribution & reach, sell multiple products,

focus on risk management and invest in people"

Sanjay Nayar

Country Head, Citibank |

Anybody who

has a Citibank credit card will know why the bank is so profitable.

Jokes apart, Citi is a lean, mean machine that pumps bucket-loads

of profits. Productivity as measured by business per branch

(Rs 1,681.9 crore), operating profit per employee (Rs 60 lakh)

and operating profit per branch (Rs 61.7 crore) are significantly

higher than the next most productive bank: ABN Amro. One of

the main reasons for the bank's high productivity is its small

number of employees-just 2,018 spread over 25 branches. That

apart, it leverages technology to lower costs and increase customer

stickiness. But it's not just profits. The bank has improved

overall to make a comeback on the list to the #2 position from

#7 last year. |

The Safest Bank

HSBC maintains its leadership here. |

|

"HSBC (#7) has big plans

for India. It already owns 14.7 per cent of UTI Bank,

and is waiting to increase its stake"

Niall S.K.

Booker

CEO, HSBC |

HSBC is the safest bank in India

for the second year in a row. The key parameters considered

to assess safety are capital adequacy ratio (car) and loan loss

cover or the provisions for non-performing assets (NPAs) as

a percentage of NPAs. HSBC has a car of 14.5 per cent (12.9

per cent for the industry) and loan loss cover of 83.8 per cent.

HSBC's NPAs as a percentage of net advances are less than one,

as against an industry average of 2.9 per cent last year. Kotak

Mahindra Bank too scores high on safety parameters, but it starts

on a low base and is just one-and-a-half-year-old. Among the

public sector banks, Corporation Bank scores high on safety

parameters. Clearly, being a bit conservative pays. |

With the Reserve Bank of India pushing banks

to conform with Basel II norms, which require higher capital adequacy

and stricter provisioning for NPAs, there'll be greater pressure

on India's banks to become more efficient. And as they battle for

market share, many will seriously consider mergers and acquisitions

as the way to go. In fact, the first of the PSU consolidations is

likely to happen between Bank of India (#34) and Union Bank of India

(#33), to create a public sector giant with Rs 1,40,000 crore in

assets. Recently, IDBI converted itself into a bank and in the last

quarter of the current financial year, IDBI Bank is to merge with

it. Says M.S. Kapur, Chairman and Managing Director, Vijaya Bank,

who has been talking of consolidation for the last two years: "Our

aggressive forays into retail and thrust on expanding loan assets

were strategies to sustain our profitability, knowing fully well

that treasury profits are a temporary phenomenon."

Banks, even if they are large, should keep

in mind that balance sheet strength alone is not going to help them

in the future. Yes, size will help, but it will not make up for

the lack of marketing nimbleness. Greater market share will be an

asset, but the efficiency of operations and quality of assets will

be more valued. And those that get this equation right will move

up not just on the BT-KPMG annual survey, but also bourses. A fact

that the country's biggest bank, the State Bank of India, will discover

from this year's survey. It has plunged from #19 to #36, not because

its performance deteriorated last year. Rather, the other banks,

most of them several times smaller than SBI, have vastly improved

their own performance.

The message from this year's survey: While

growth is crucial, the quality of it is even more so. Global Trust

Bank learnt that the hard way. Let's hope the other weaker banks

get the message before it is too late.

|