|

| Hutch's Asim Ghosh: He's on shortly |

It

needs to prove that

its pure-play mobile-telephony business model is as good as the

integrated one preferred by most telcos. And it needs to disprove

the theory about its inability to grow in smaller cities and rural

areas. At stake are a shot at telecommunication greatness and a

slice of the second most happening telecommunications market in

the world. By Priya Srinivasan

It sounds more complex than the shareholding

pattern in reliance," laughs the telecom analyst at a Mumbai-based

brokerage. His reference is to the centrepiece of the spat between

the Brothers Ambani, the 29 per cent stake in Reliance held by a

web of holding companies-the stake that one brother implies he controls.

And he is talking about Hutchison Essar, the company whose creation

has just been cleared by the Ministry of Finance. "The company

will probably spend the entire analysts' meeting explaining it,"

he adds.

The facts first: the finance ministry comes

into the picture because Hutch is a foreign company (Hutchison Telecom

International Limited or HTIL, promoted by Hong Kong-based tycoon

Li Ka Shing) and Indian laws are very particular about how much

of a telecom company a foreign corporate can own (the ceiling for

foreign direct investment is 49 per cent). The government chooses

to turn a blind eye to indirect ownership-for instance, company

A can own 49 per cent in telco T directly; the remaining 51 per

cent can be held by a joint venture in which Indian company B owns

51 per cent and A owns 49 per cent; thus, the total 'economic' stake

of A in T becomes 73.01 per cent-but with HTIL set to own 42 per

cent in Hutchison Essar directly, and 14 per cent indirectly, the

new structure needed to be cleared by the Ministry of Finance.

And the bit about the analysts comes into the

picture because Hutchison Essar plans to make an initial public

offering (IPO) in the next six to eight months. Already, discussions

on new public offerings on online bulletin boards of brokers and

traders in India are dominated by talk of the impending Hutchison

Essar IPO. Everyone's appetite has been whetted by the disclosure

of the financial details of the Indian subsidiary necessitated by

htil's recent IPO (it was listed on the Hong Kong exchange in October),

numbers impressive enough for stock traders, analysts, investment

bankers, lead managers and sundry entities allied to the stock markets

to embark on their own number-crunching exercises to make a pitch

for an offering that would make their books look good. "Every

lead manager in the business is preparing a pitch," says a

telecom specialist at a local investment bank.

| The Rivals |

Mukesh

Ambani Mukesh

Ambani

Reliance Infocomm

Subscribers as on November 30: 9.8 million

He and his company have been in

the news for other reasons, but Reliance Infocomm remains India's

biggest mobile telephony company. That, and money-power, make

it a formidable rival.

Sunil

Mittal Sunil

Mittal

Bharti Tele-Ventures

Subscribers as on November 30: 9.41 million

He has outsourced key functions

such as network ownership and management, and IT, and Bharti

has the enviable record of having its investments in infrastructure

pay off in record time.

A.K.

Sinha A.K.

Sinha

BSNL

Subscribers as on November 30: 8.15 million

His company operates in 22 circles,

but is strapped for resources given that its primary businesses

still remain national long distance and fixed line telephony.

Ratan

Tata Ratan

Tata

Tata Teleservices, VSNL

Subscribers as on November 30: 2.1 million

He was late to the CDMA-party

but his company has since made some gains. The acquisition

of Tyco's undersea cable and the effort to target enterprises

with a bundled service could catapult it into the big league.

|

The numbers warrant that: in the six months

ended June 30, 2004, Hutchison Essar registered a turnover of Rs

1,888 crore, 46.5 per cent of HTIL's revenues of Rs 4,064 crore

for the same period (the single largest chunk). And in 2003, the

company (Hutchison Essar) did business worth Rs 2,652 crore. The

IPO, when it happens, will be everyone's chance to grab a piece

of the most happening market in India, mobile telephony; that's

a rare opportunity. Barring Bharti Tele-Ventures, VSNL, MTNL, and

part of Tata Teleservices, there are no investing opportunities

for equity investors in telecom.

Paradoxical as it may sound, the new holding

structure is far simpler than the old. Hutchison Essar, explains

an investment banker in the know, "will be a listed company"

in which all partners (HTIL, the Hinduja Group, the Max Group, Essar

and financial investor Kotak Mahindra) hold shares and the other

companies, the ones operating across circles under the Hutch umbrella,

will be "100 per cent subsidiaries". The old structure

involved six independent companies, Hutchison Max, Hutchison Essar,

Hutchison Telecom East, Fascel, Hutchison Essar South and Aircel

Digilink, with HTIL's stake (direct and indirect together) ranging

from 42 per cent to 56 per cent (then, the company's service offering

in Mumbai, its single biggest operation, is branded Orange). And

as the name of the new entity indicates, the Essar Group is the

second largest shareholder in the company, with a 30 per cent stake.

Indeed, the Ruias of Essar seem to be getting their second wind

in telecom, as their acquisition of France Telecom's 9.9 per cent

stake in BPL Mobile Communica-tions, the company that provides mobile

telephony services in Mumbai shows. That, though, is another story.

And complex holding structure or not, there can be no arguing the

fact that Hutchison Essar (Hutch, for short) is a company to watch.

The obvious reason behind the interest in Hutchison

Essar is its impressive numbers. Telecommunications is still a nascent

enough industry in India to be measured by EBITDA (earnings before

interest, taxes, depreciation and amortisation)-the logic being

that companies operating in sectors that are as capital intensive

as telecom will, in their early years, find their post-tax profits

weighed down by interest (on debt that funds capital expenditure),

depreciation and amortisation. "It will be at least another

year before we start valuing telecom companies purely on net earnings,"

says Prahlad Shantigram, Managing Director (Corporate Finance and

Advisory), Standard Chartered, who, in his previous avatar as head

of investment banking at DSP Merrill Lynch, lead-managed Bharti

Tele-Ventures' January 2002 IPO.

On the basis of this parameter, Hutch's operating

margins currently stand at around 34 per cent while Bharti's, for

its mobile telephony business (the company is also into national

and international long distance telephony, although mobile telephony

accounts for 70 per cent of its revenues), is comparable at 34.25

per cent for the six months ended September 30, 2004. While Hutch

still hasn't publicised its detailed profit and loss account (something

that would make a more elaborate comparison of the two telcos possible),

investment bankers in the know suggest that its net profit margins

could be a couple of percentage points higher than Bharti's. That

is only to be expected given the latter's integrated play. "Companies

such as Bharti have much higher depreciation and interest costs,

and these show up in their net margins," says another investment

banker. "I wouldn't be surprised if Hutch's net profit margins

are better." Then, there are analysts who are convinced that

better isn't better enough. Priyanko Panja of Edelweiss Capital

is one such; he believes Hutch's costs are higher than they should

actually be because it doesn't own its own NLD (national long distance)

and ILD (international long distance) infrastructure, choosing instead

to buy bandwidth from companies in this business. That opinion is

just the tip of the unresolved debate on the better business model:

some insist it is integrated play; others, an equal number, are

certain it is pure play.

|

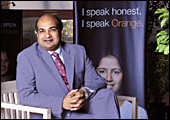

| Hutch's Deputy Sandip Das: Hutch, Orange,

whatever it takes to get close to customers |

Creating Solid Business

Hutch's distinguished-looking Managing Director-that's

what a mane of shocking white hair does to most people-Asim Ghosh,

for one, is convinced that both fly. "Ours is a solid business

in its own right and I don't see much merit in (Hutch) being compared

with the competition that has a fine business in its own right."

The man's right, of course: ILD and NLD are high margin services;

then, they require substantial investment. "We clearly do not

view the situation as one where 'If it's telecom, we have to be

in it'," says Ghosh. "I am interested in creating a solid

consumer business." There are enough buyers for that argument.

"End-customer businesses where you can determine price points

and offer differentiated services always command a premium over

intermediary businesses," says Salil Pitale, Vice President,

Enam Financial Consultants. "In a geographically vast and competitive

market like India, there is an edge that integrated players have,

but that is not to say a company cannot thrive as a mobility player,

and companies such as Vodafone are standing examples of this,"

adds Kobita Desai, Principal Analyst (Telecom Services and Mobile

& Wireless Communications), Gartner.

Strangely enough, the one argument that challenges

Hutch's pure-play business model comes from its greatest strength,

marketing. At the boardroom at Hutch's snazzy central Mumbai headquarters,

there are five awards on display; three of these have to do with

marketing and advertising. "Hutch recognised early on that

it is in a service industry and not a technology industry,"

says Renuka Jaypal, National Business Director, Ogilvy & Mather,

the agency that handles all the company's advertising. The results

of that understanding are evident in two things: the preference

corporates have traditionally shown for Hutch, and its high average

revenue per user (ARPU), the highest in the industry.

The problem is, rivals such as Bharti, Reliance

Infocomm and the Tata Group, all integrated players, are aggressively

targeting corporates with the kind of bundled offerings that only

an integrated player can offer. And that could hurt Hutch although

Ghosh says that, "we will do whatever it takes to service customers".

National-level Player?

The other challenge that Hutch faces also has

to do with its high arpu. This, reason competitors, has been built

on the back of a metro and large-city focus. "The real question

is, does Hutch stand a chance of being a national player in the

league of Reliance, Bharti or bsnl with a pan-Indian footprint?"

asks an executive at a rival telco. "Can it compete with its

limited metro A and B profile?"

Thus far, it has. Hutch currently operates

in 13 circles and hopes to grow its subscriber-base at the same

rate as the industry (85-100 per cent). And with 6.85 million subscribers

(as on November 30, 2004), it compares favourably with Reliance

(9.8 million), Bharti (9.41 million) and BSNL (8.15 million).

The future, though, could be an entirely different

ballgame as Gartner's Desai points out: " Volumes are most

likely to come from B and C circles where Hutch has a limited presence,"

she says. "It is unlikely to garner the volumes of a Reliance

or a Bharti." Ghosh himself will only say that "the management

of individual circles and their financials is crucial", but

chances are, he will be as happy with 12 million high-end subscribers

as with five million high-end ones and 15 million low-end ones.

Hutch, after all, is widely seen as the leader in value-added services

and apart from contributing to the company's revenues, according

to Ghosh, "it is also the reason we attract high-end subscribers".

Fact is, Hutch is also making a bit of volume

play, largely through acquisitions. However, its acquisition of

Aircel, the cellular service provider in Chennai and Tamil Nadu,

is stuck in limbo, although it was announced way back in June 2004.

Will the lack of volumes hurt, or will investors recognise the company's

value-play? We will have to wait for 2005 to answer that.

|